There’s a trucker out of Missouri who did everything right—on paper. He registered with the FMCSA, bought the proper liability coverage, paid his BOC-3 filing fee, and even had his authority granted. Business kicked off fast. He leased a reefer, picked up some grocery freight, and was rolling into six states by the end of month two.

Then, the letter came.

His authority was being suspended. Why? A missing federal form—an MCS-90 endorsement. It wasn’t malicious. It wasn’t even negligent. He just assumed the insurance policy he paid for had him covered.

It didn’t.

This happens more often than most trucking companies realize. Not because truckers are careless, but because federal insurance regulations aren’t exactly written in plain English. Some rules aren’t enforced until it’s too late. Others live in gray areas of jurisdiction between FMCSA, DOT, and state-level insurance boards.

But forgetting even one of these requirements can freeze a business overnight.

This article isn’t about the insurance you already know. It’s about the stuff that gets forgotten—the dusty filings and strange acronyms that sit just below the surface of compliance. The ones that can make or break your authority.

Let’s start with the basics—because even the basics come with fine print.

If you’ve been around the trucking block, you’ve probably heard this one:

“You need at least $750,000 in liability coverage to operate.”

Technically, true. But the FMCSA's insurance minimums depend on a few variables:

Here's the breakdown:

So far, so good, right?

Most carriers get this part right. But here’s the trap: having the right policy limits doesn’t mean the feds know you’re compliant.

That’s where the filings, endorsements, and specialized coverages come in—things that aren’t necessarily sold in the average policy, but are required by federal regulation.

This is where trucking insurance gets tricky. You can be insured and still be non-compliant. And no one will tell you… until your authority vanishes.

Most carriers think compliance is a one-time checklist. You get your MC number, buy a liability policy, file the BOC-3, and you're golden.

But there’s a second layer—the quiet side of federal compliance. It’s full of acronyms, weird forms, and assumptions that can blow a hole in your business if you’re not paying attention.

These are the most commonly forgotten federal insurance requirements—the ones that get overlooked until the fines start stacking or a broker won’t dispatch you because your FMCSA profile has a red flag.

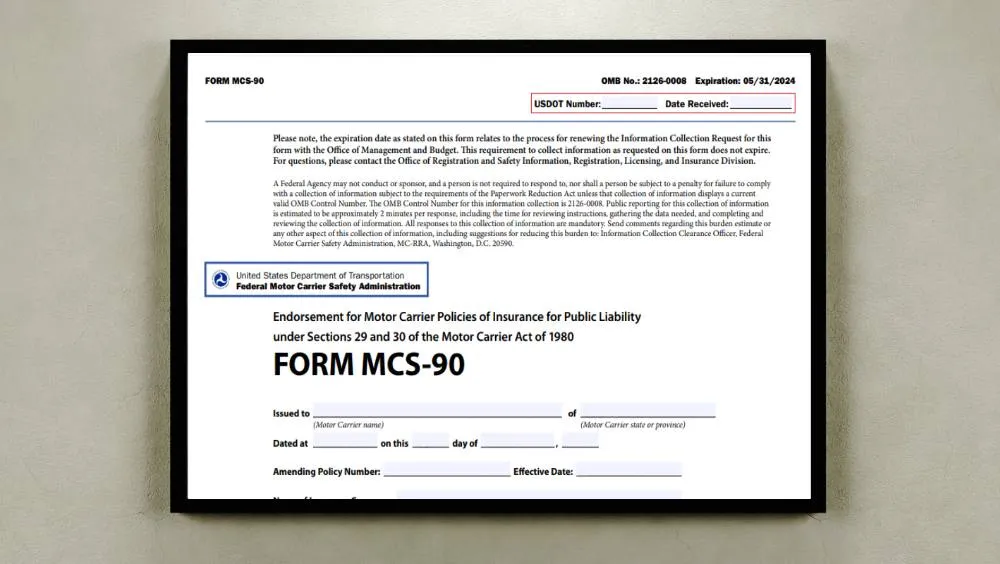

Here’s the irony: the MCS-90 isn’t even an insurance policy. It’s an endorsement—a slip of paper that attaches to your liability policy and says, “Yes, we’re federally compliant. We’ll cover damages even if the policy technically says otherwise.”

So what’s the big deal?

Well, the MCS-90 is the government’s safety net. If you crash and your policy doesn’t cover it for some fine-print reason (like a hazmat exclusion), the MCS-90 forces the insurer to pay anyway.

It’s essentially the insurance company guaranteeing the public will be made whole, no matter what.

Why it's forgotten:

Most carriers assume it’s included automatically. But many insurers don’t add it by default, especially if they’re unfamiliar with trucking or you’re bundling different types of coverage.

Why it matters:

You could have a million-dollar liability policy and still lose your operating authority if the FMCSA doesn’t see the MCS-90 on file.

Don’t assume. Check your declarations page and filings.

The BMC-91 (or its cousin, BMC-91X) is not an insurance policy. It’s proof to the FMCSA that your insurance meets the federal minimum.

You’d think your policy alone would be enough. It’s not.

Here’s how it works:

These forms are filed electronically by your insurance company. If they don’t file them (or mess it up), your FMCSA record will show “INSURANCE NOT FILED”, even if you paid thousands in premiums.

Why it's forgotten:

New carriers, especially those using out-of-state agents or online platforms, may not realize this filing is their lifeline. Some agents just issue the policy and walk away.

What it costs you:

Your authority can be revoked or delayed indefinitely while your filings sit in limbo. We’ve seen carriers miss out on big contracts or have their trucks parked for weeks over this.

Solution:

Work with an agent who doesn’t just sell you insurance—but actually files your BMC forms with the FMCSA.

Most people think the worst part of a trucking accident is the collision.

It’s not. It’s the spill.

If you’re hauling anything remotely hazardous—fuel, chemicals, even large quantities of batteries—and something leaks during an accident, you’re not just on the hook for damages. You’re on the hook for environmental cleanup.

That’s where Environmental Restoration coverage comes in.

Why it’s forgotten:

It’s often not included in standard policies. Many carriers don’t realize that if their load spills into a waterway or soil, the EPA can bill you six figures for restoration. And they don’t wait around for your insurance to figure it out.

Who needs it:

Fun fact (not fun at all): The DOT’s definition of a “pollutant” is broad enough to include milk, depending on the volume and circumstances.

If you’re moving anything that could spill, seep, or corrode—check your policy. Environmental Restoration is often the difference between a bad day and a business-ending one.

You’re a carrier, not a broker—right?

Maybe. But a lot of small carriers dip into brokering from time to time. They pass a load to a friend. They book a backhaul for another driver. Or they set up a separate MC number for brokerage without realizing the compliance side of it.

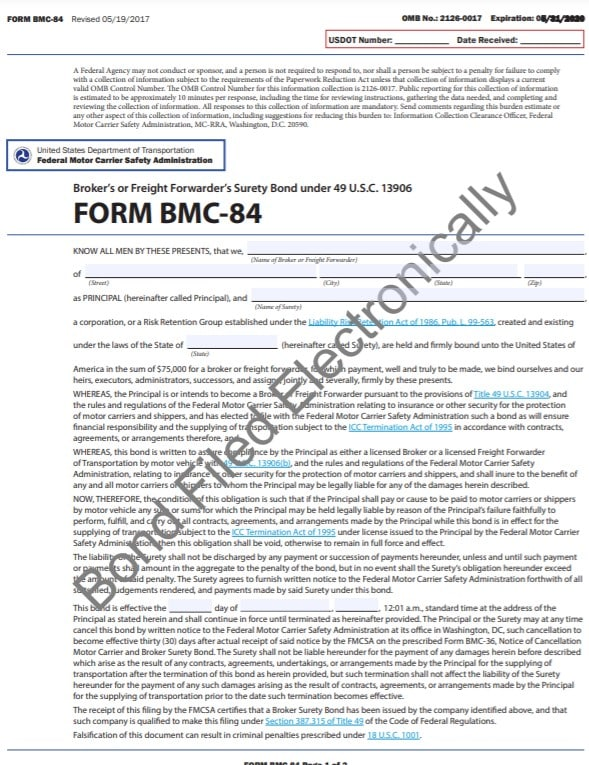

If you broker freight—even once—you’re legally required to have a $75,000 surety bond (or a trust fund), filed with the FMCSA via BMC-84 (or BMC-85 for the trust version).

Why it’s forgotten:

Many carriers think brokering a load is just a phone call. It’s not. It’s a federally regulated activity that triggers a completely different set of requirements.

Without the bond, your brokerage authority is invalid. Worse, you could be accused of double-brokering, which gets you blacklisted faster than a low credit score.

Why it matters:

Brokers are under heavy scrutiny right now. Carriers who think they’re just “helping out a friend” can get caught in a compliance nightmare.

If you're brokering loads, even casually, make sure you're bonded. And make sure it's filed properly with the FMCSA—this isn’t one you can fake.

Here’s the paradox: Workers’ comp isn’t federally required for trucking.

But also… yes, it is. Sort of.

Let me explain.

At the federal level, the FMCSA doesn’t enforce workers’ comp mandates for carriers. But if you:

…then suddenly it’s required.

Where this really trips people up is multi-state operations. A carrier based in Texas might run loads into California, where the rules are wildly different. California doesn’t care what your home state says. If you’re operating there and something goes wrong, they want to see workers’ comp.

Why it’s forgotten:

Because it’s not enforced until someone’s injured. Then the lawsuits start. And if you don’t have coverage, you’re on the hook personally.

What it costs you:

Medical bills, legal fees, possible civil penalties—and in rare cases, criminal charges for non-compliance.

Solution:

If you’re unsure whether you need it, assume you probably do. Especially if you have W-2 drivers or you’re bidding on any government contracts.

If you’re not doing intermodal work, this won’t matter.

But if you’re hauling containers, especially from ports or rail yards, the Uniform Intermodal Interchange and Facilities Access Agreement (UIIA) is your gatekeeper.

.png)

Think of it like a country club for ports. No membership? No entry.

UIIA requires:

Each terminal has its own flavor of rules—but they’re all backed by the UIIA.

Why it’s forgotten:

Because it’s not an FMCSA thing. It’s not on your MC profile. It lives in the logistics world, not the federal one.

What it costs you:

You show up at the port with a chassis-ready truck, and the terminal security says “You’re not listed.” Now your driver sits unpaid, your load is delayed, and the broker starts calling other carriers.

Pro tip:

If you're planning to enter the intermodal space, get your insurance agency to preload your certificates into the UIIA system. You’ll thank yourself later.

Here’s a scenario:

A leased-on driver drops off a load, deadheads back, and hits a car on the way home. Whose insurance pays?

Most carriers and drivers say “Non-trucking liability,” or NTL.

But what they often really need is Bobtail coverage—and the difference matters more than you think.

NTL covers personal use when not under dispatch.

Bobtail covers you anytime the truck is being driven without a trailer, regardless of whether you're under dispatch.

Why it’s forgotten:

Because agents outside of trucking often mix them up, and carriers assume they’re the same thing. They’re not. Courts have ruled on this over and over.

If your driver causes an accident and you’ve got the wrong coverage, both your company and the driver might be left holding the bag—especially if someone’s injured.

Here’s the bottom line; get clear on when your trucks are covered and for what. The dispatch line is blurry, and you do not want to argue it in court.

Say you're pulling someone else’s trailer under a trailer interchange agreement.

You’re not leasing it. You’re not borrowing it casually. You’re exchanging it under a formal agreement, which makes you financially responsible for any damage.

Most general liability policies do not cover the trailer itself if you don’t own it.

That’s where Trailer Interchange coverage comes in.

Why it’s forgotten:

Because carriers assume their cargo insurance or auto liability has it covered. It doesn’t.

What it costs you:

A scraped or overturned trailer that isn’t yours? That’s your bill now—thousands, possibly tens of thousands if it's damaged during a load.

Also, some ports and intermodal carriers require this coverage before they even load your truck.

This is the trickiest policy on the list.

If you’re using owner-operators or 1099 drivers, you legally can’t provide them with workers’ comp unless they ask for it—and they often don’t. So instead, you need Occupational Accident (Occ Acc) coverage.

%20coverage.png)

It’s not federally required. But…

Why it’s forgotten:

Because it’s not on any FMCSA checklist. But it’s a practical necessity if you want to stay out of legal hot water and remain broker-friendly.

What it costs you:

Lawsuits, reputational damage, and potential liability payouts that your commercial insurance won’t cover—because the driver wasn’t technically an employee.

The fix:

If you’re using leased drivers, Occ Acc coverage should be standard. It's cheaper than workers’ comp and designed for the 1099 world.

There are moments in trucking where your insurance obligations suddenly multiply—quietly, and without warning. You might not even realize it happened until your paperwork’s rejected or a fine shows up in the mail.

Here are some federal edge cases where your requirements change based on what you haul, where you go, or how your operation is structured.

The moment your wheels cross an international line, the game changes. You’ll need:

Canadian and Mexican authorities may have their own insurance verification steps—and failure to comply can mean getting turned around at the border or delayed in customs for hours.

Everyone knows hazmat is risky. But the part most forget? The insurance requirements spike instantly.

If hazmat is even occasionally part of your operation, build your policy as if it's always there. That’s how regulators treat it.

If you carry passengers instead of freight, your requirements are a completely different universe:

This includes party buses, tour vans, employee shuttles—anything that moves people for hire.

Many small operators fall into this trap: they run a "courtesy shuttle" without realizing it qualifies as passenger-for-hire, triggering entirely different compliance standards.

Moving someone’s couch across state lines? The FMCSA considers that consumer cargo, and it’s protected under specific federal rules that don’t apply to regular freight.

You’ll need:

And don’t expect to hide under a freight policy. If a family complains to the FMCSA or DOT, they’ll come knocking fast.

Non-compliance doesn’t always look like a dramatic roadside inspection or a courtroom battle. Sometimes it’s quieter—and more expensive in the long run.

Let’s break down what really happens when a federal insurance requirement gets missed.

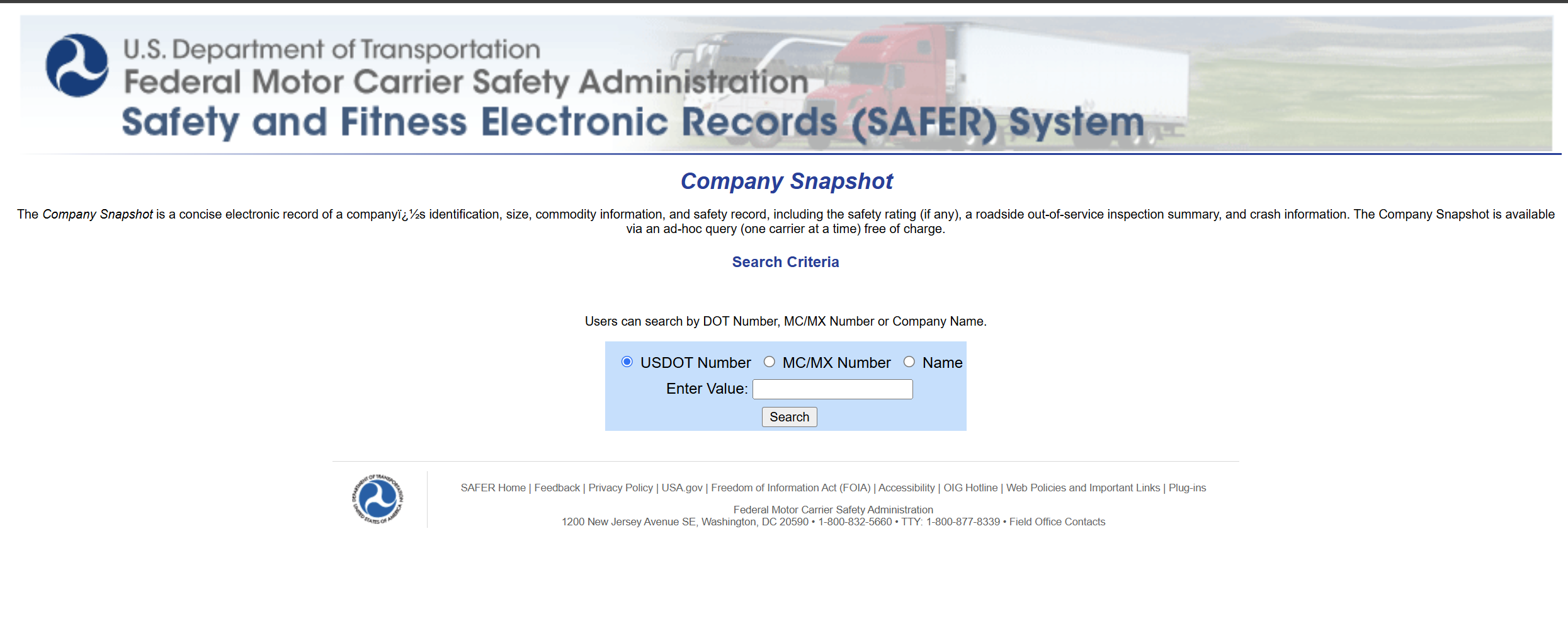

You could get red-flagged by the FMCSA.

Every broker, shipper, and safety manager you work with can see your compliance status on SAFER and Carrier411. One missing filing and you might as well have a “DO NOT LOAD” sign taped to your MC number.

There could be delays in authority activation or renewal

We’ve seen carriers wait weeks or months to get their authority active simply because their BMC-91 wasn’t filed right. In trucking, that’s lost revenue—every single day.

Next, fines and civil penalties.

Miss a required filing or operate under the wrong coverage? The FMCSA can hit you with $1,000+ per violation per day. And they’re not shy about it.

Hazmat? The penalties multiply—up to $75,000 per violation, and more if there's injury or environmental damage.

Denied claims and lawsuits

This is the gut punch. You get in an accident, file a claim, and the insurer says:

“This wasn’t covered under your current policy.”

Now you’re paying out of pocket—or worse, fighting for your business’s survival in court.

Loss of broker or customer relationships.

Brokers are checking your insurance profile before they even call you. If something’s missing or outdated, you’re not getting the load—simple as that. Shippers don’t call back. Port gates stay closed.

Compliance isn’t just legality—it’s revenue protection.

Most of the mistakes we’ve covered aren’t about bad intentions. They’re about bad assumptions. That’s fixable.

Here’s how smart carriers keep it tight.

This is non-negotiable.

A generalist agent might get you cheap premiums—but they won’t know about trailer interchange clauses, BMC filings, or how to keep your UIIA access active. Find someone who lives in the trucking space and handles FMCSA filings as part of the deal. Like us! Visit allcapitalinsurance.com/contact to learn more.

At least once a year (preferably every six months), do a full audit of:

You’d be shocked how often companies outgrow their coverage and don’t realize it until a claim is denied. If this sounds too tedious, there are companies such as All Capital Compliance that could do this automatically for you.

Check your SAFER record like you check your bank balance. One bad filing can block loads or trigger a warning from the DOT. Make it routine.

Any time your business changes—new truck, new driver, new lane, new cargo—have a protocol in place. One that checks:

This turns surprises into small updates instead of costly mistakes.

The biggest risk in trucking isn’t the weather, or the roads, or even the freight.

It’s what you assume you’re covered for… and aren’t.

We’ve seen too many good carriers go dark because of one forgotten filing. One missed endorsement. One policy that didn’t get updated when the business changed. And the worst part? It wasn’t carelessness. It was trust—trust in a system that rarely explains itself.

Federal insurance compliance isn’t a checkbox. It’s a living, breathing part of your operation. And it doesn’t give warnings. Just consequences.

But here’s the good news: you don’t have to figure it out alone.

At All Capital Insurance, we don’t just write trucking policies. We build shields—the kind that cover you on paper, in court, and everywhere in between. We handle the filings, flag the gaps, and help you stay on top of the rules before they turn into problems.

If you’re not sure whether you’re fully covered, or you just want a second set of eyes on your filings, let’s talk. A 15-minute review could save you thousands in fines—or a phone call you never want to get from the FMCSA.

No pressure. Just real answers from people who know trucking inside and out.

Schedule a free compliance check today.

Let’s make sure your business is bulletproof.

Insurance Filing Requirements FMCSA detailed insurance filing needs

MCS-90 Endorsement Definition Requirements Who Needs It

Understanding FMCSA Insurance Requirements minimums and updates

FMCSA Insurance Requirements for Commercial Vehicles form details

Form MCS-90 Endorsement for Motor Carrier Policies legal text

49 CFR Part 387 minimum financial responsibility levels

Frequently Asked Questions FMCSA insurance update processes

Federal Motor Carrier Safety Administration safety and compliance